Avoid Common Medicare Mistakes

You’ve probably heard your neighbor or friend complain about Medicare at some point and say how crucial it is to get Medicare right on the first try. Today, we’ll discuss some of the common mistakes seniors often make when starting Medicare or turning 65.

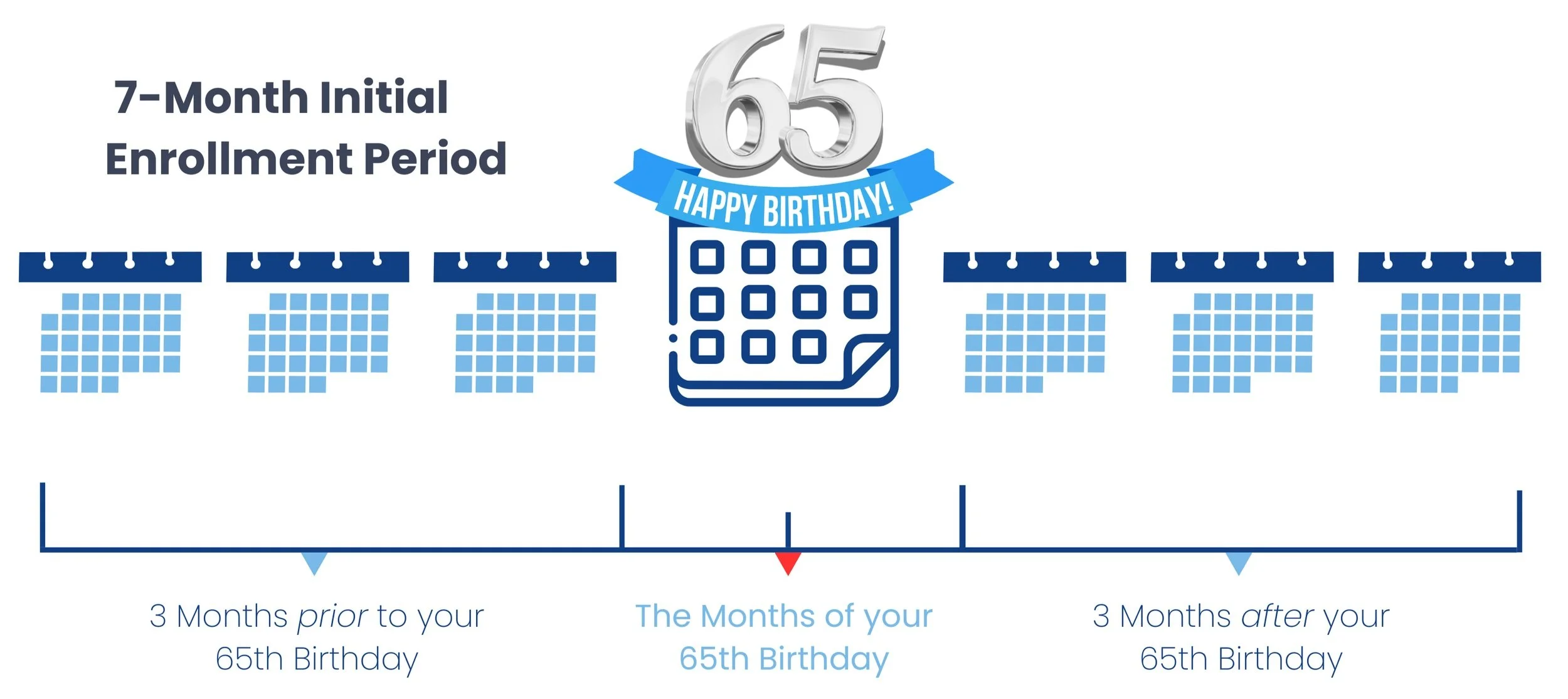

Missing the Initial Enrollment Period

Missing the Initial Enrollment Period is likely the most common mistake seniors make when turning 65. When you turn 65, you are eligible for Medicare through the Initial Enrollment Period. The Initial Enrollment period spans 7 months which include the 3 months prior to your 65 birth month, the month of your 65 birthday, and the 3 months after your 65 birth month.

Should you enroll in Medicare when you turn 65? That depends on your specific circumstance. Failing to have creditable coverage and missing your Initial Enrollment Period will result in a 10% penalty per year, paid for life! Similarly, the Part D penalty is 1% per month without creditable coverage. Continue reading about the Initial Enrollment Period here.

Note: If you are actively employed and offered group health insurance, enrolling in Medicare may not be the best option for you. However, you should consult a Medicare expert prior to turning 65.

Not Understanding Coverage Gaps

What are coverage gaps? A coverage gap refers to the financial risk or lack of protection left by a health insurance plan when certain services or expenses are not covered. Beneficiaries who enroll in Original Medicare without Medicare Supplement or Medicare Advantage will experience coverage gaps. Original Medicare covers 80% of Medicare approved services leaving you responsible for the remaining 20%. That’s 20% of medical costs with no maximum-out-of-pocket. With a Medicare Supplement, Medicare pays 80% of medical costs and the Supplement pays the remaining 20%. No coverage gap. Medicare Advantage offers beneficiaries a maximum out-of-pocket which is the most they will have to pay for medical costs in a year before the plan covers all additional expenses. Original Medicare by itself often leaves unwanted financial risk. Be sure to shop for a Medicare Supplement or Medicare Advantage plan to avoid coverage gaps in your health insurance.

Not Reviewing Their Medicare Plan

Medicare Advantage and Prescription drug plans should be reviewed each year to ensure you are still on the best plan for your situation. The time to review your Medicare Advantage or Prescription Drug plan is known as the Annual Enrollment Period (October 15 - December 7). During this enrollment period, you can review the changes coming to your plan for the following year. When reviewing your plan, you should considering changes in your premium, deductible, maximum-out-of-pocket and copays.

According to an KFF analysis, 82% of Medicare Advantage beneficiaries did not review their plan in 2021 for the new year. Similarly, 69% of Prescription Drug beneficiaries did not review their plan for 2022. Each Medicare Advantage and Prescription Drug Plan has a list of covered medications which is known as a formulary. These formularies often change each year. Thus, confirming your medications are covered by the plan’s new formulary is highly recommended.

Medicare Advantage Review in 2021

Prescription Drug Review in 2021

Medicare has various angles and offers many opportunities for mistakes. Our discussion only covered a few of the most common mistakes made by Medicare beneficiaries.

Ways to avoid Common Medicare Mistakes are:

1) Educate yourself on the basics of Medicare. Attend a Medicare seminar where you can learn first-hand from a live expert.

2) Ask someone for help. Agents and Brokers are available throughout the States and are willing to assist in your situation.

3) Learn from the experience of others. Ask your friends about their experience starting Medicare.